Alternative Real Estate Investments: Medical, Senior, and Student Housing

Investors are increasingly looking beyond traditional offices, retail centers, and apartments to alternative real estate sectors that offer stable, long-term growth. In particular, medical facilities, senior housing, and student housing are underappreciated asset classes with strong demand drivers and inherent supply constraints. These sectors benefit from long-duration leases or recurring usage, and they tap into powerful demographic trends. High demand and limited supply can translate into resilient occupancy rates and potentially above-average returns for investors willing to diversify into these niches. The following report provides a global overview of these sectors – emphasizing the U.S., Europe, and Asia – and explains the investment thesis behind each, including recent case studies and data illustrating their performance.

Senior Housing: Demographic Tailwinds and Limited Supply

Demand Drivers: Senior housing (including independent living, assisted living, and nursing care facilities) is bolstered by an aging population and increased longevity. The U.S. is a prime example: the cohort aged 80 and over is projected to grow by 36% in the next decade, creating a sizable wave of potential residents for senior living communities. Similar trends are evident in Europe and parts of Asia. In fact, Europe’s population aged 80+ is expected to jump 35% by 2032, and countries like South Korea became “super-aged” in 2024 with 20% of the population over 65. These demographics underpin persistent demand for senior housing well into the 2040s. Seniors often require housing with care services, making this a needs-based sector (less discretionary than hotels or offices) and providing relatively stable demand even during economic cycles.

Supply Constraints: Despite growing demand, the supply of quality senior housing is constrained by high development costs, lengthy zoning and licensing processes, and a historical undersupply in many regions. In Europe, the senior housing and care market remains fragmented and undersupplied, which has traditionally kept occupancy rates high and drawn investor attention. In Asia, governments are only starting to incentivize development – for example, South Korea has introduced policies to support senior housing due to a “critical shortage in both the quantity and quality” of options. This limited supply relative to a rapidly growing elderly population creates an environment of high occupancy and the ability for operators to raise rents or fees steadily. Investors also see opportunities to acquire or develop facilities below replacement cost in some markets, capitalizing on this supply-demand imbalance.

Investment Thesis: Senior housing offers investors long-duration income streams and potential for above-average yields. Many properties operate under triple-net leases or management contracts with experienced operators, often spanning 10 to 20 years. This means steady rent payments and lower turnover compared to traditional apartments. Long-term demographic trends act as a tailwind, and the sector’s performance has started to reflect that. Even after pandemic challenges, senior housing is rebounding strongly: one industry survey found the majority of investors plan to increase exposure to seniors housing in 2025, with only 2% looking to decrease. Investors anticipate cap rate compression (rising values) in this sector as competition for limited assets heats up. In 2024, senior housing and care property sales surged to $13.2 billion in the U.S., up 21% from 2023 – a clear sign of renewed investment appetite. Importantly, leading healthcare REITs reported exceptional property performance: for example, Ventas’s seniors housing portfolio saw nearly 16% same-store NOI growth in 2024, and Welltower’s senior housing portfolio logged almost 24% NOI growth in Q4 2024. These gains were driven by rising occupancy and rents, showcasing the sector’s ability to generate growing cash flows as it recovers.

Case Study – Institutional Investment: Large institutions are actively investing in senior living. In late 2023, Morgan Stanley Real Estate Investing acquired a portfolio of eight senior housing communities (1,186 units) from developer Harrison Street. The properties – located across major East Coast markets – continue to be operated by a top-tier senior living company (Brightview Senior Living). Harrison Street, a leading investor in this space, has invested around $14.5 billion across 42,000 senior housing units to date. This case illustrates both the scale and confidence of institutional investors in the long-term prospects of senior housing. Similarly, in Asia, private equity firm Warburg Pincus formed a joint venture in 2025 to develop senior housing in Seoul, citing “tremendous opportunities fueled by shifting demographics” and government support in a market where seniors now make up 20% of the population. These examples underscore a growing consensus: senior housing, once a niche real estate play, is becoming a mainstream investment category thanks to its durable demand drivers.

Student Housing: Resilient Demand and Chronic Undersupply

Demand Drivers: Student housing – especially purpose-built student accommodation (PBSA) near universities – has proven to be one of the most resilient real estate sectors. Demand is anchored by higher education enrollment, which in many countries has a long-term uptrend. Global mobility for education is also rebounding, as international students seek degrees abroad. In 2024, the student housing market in major study destinations had a banner year thanks to surging international student demand. Notably, the sector is so undersupplied that even if there were temporary dips in enrollment, occupancy would likely remain robust. In the U.K. (one of the largest markets for international students), demand far outstrips supply, with cities like London facing the widest gaps between student populations and available beds. Across Europe, most top university cities see more student demand than housing supply, driving occupancy rates above 95% in many PBSA facilities. The U.S. likewise benefits from large domestic student populations and steady international inflows; large “Power 5” universities are experiencing record enrollment and have become magnets for new private student housing developments. On a global scale, the rise of a wealthy middle class in developing countries has expanded the pool of students who can afford international education, further fueling demand for accommodation. In short, enrollment growth and mobility trends ensure a growing tenant base for student housing year after year.

Supply Constraints: Supplying student housing is not easy, contributing to persistent shortages. Universities often have limited land or capital to build new dormitories, so private developers step in – but they face zoning hurdles, high construction costs, and community resistance in some college towns. It can take years to plan and build new PBSA projects, and in the meantime student numbers continue to grow. In the U.S., some campuses and surrounding towns have seen a wave of new beds delivered, yet demand still keeps occupancy high. In the U.K. and Europe, the situation is more acute: BONARD (a student housing research firm) reported nearly 65,000 new beds added across 131 cities in 2024, yet that was not enough to meet the excess demand. Key hubs like London and Paris have development pipelines in progress, but those cities also have the largest demand gaps to close. In many cases, the “low-hanging fruit” (easy sites for development) have been exhausted, and any new supply must overcome significant regulatory and cost barriers. Because students typically want to live near campus, location is a limiting factor – housing farther away is less attractive, so central, walkable sites are at a premium. All these factors mean that in popular study destinations, student housing occupancy is reliably high and rental rates have a strong floor.

Investment Thesis: The appeal of student housing to investors lies in its stable occupancy, predictable turnover, and attractive yields relative to conventional apartments. While college students cycle through every year or two, the apartment units (or dorm beds) are re-released to a new cohort, creating a consistent income stream if managed well. In fact, student rentals often come with parental guarantees or financial aid backing, which can make rent collection more secure. Many leases are signed for 12-month terms aligned with the academic calendar, leading to long booking cycles and high pre-leasing rates well before each school year. As evidence of the sector’s resilience: by late 2024, U.S. student housing properties were 94.5% pre-leased on average (with dozens of major universities at 99% occupancy) for the fall term. Even during economic downturns, college enrollment tends to hold steady or even increase (as people seek to upskill), which insulates demand for these properties. Rental growth has also been robust – for instance, across global markets student housing rents rose about 7.4% year-over-year in 2024, outpacing inflation in many countries. Because the sector was historically viewed as specialized, cap rates (investment yields) have been slightly higher than for mainstream multifamily, providing a spread for investors. Now, with its track record during the pandemic and subsequent recovery, student housing is attracting big capital. One industry executive called it “one of the most resilient asset types in real estate”. Over the past decade, portfolios focused on student housing have delivered solid returns, often outperforming traditional rental housing on a risk-adjusted basis.

Case Study – Growing Investor Interest: In 2024, private equity giant KKR acquired a $1.64 billion portfolio of student housing properties from Blackstone’s BREIT and Greystar. This blockbuster deal involved 19 assets across various U.S. university markets and signaled strong institutional confidence in the sector’s prospects. Other major transactions included a consortium (The Scion Group with Singapore’s GIC and Canada’s CPPIB) refinancing 11 student housing properties in early 2024 to recapitalize and expand their holdings. These deals highlight how large investors are consolidating portfolios to achieve scale in student housing. In Europe, dedicated student housing REITs and funds have also grown – for example, Unite Students in the UK and Xior in continental Europe have been expanding to meet demand. The global student accommodation market was valued around $11.3 billion in 2023 and is projected to grow at ~5% annually to $15.9 billion by 2030, reflecting both development of new projects and rising valuation of existing assets. The investment thesis is clear: as long as universities continue to attract students, especially in top-tier and English-speaking markets, well-located student housing properties should enjoy near-full occupancy and steady rent growth, providing reliable cash flows. Investors who get in early in undersupplied markets may also see appreciation as these assets become more scarce and institutionally sought-after.

Medical Facilities: Healthcare Demand and Stable Long-Term Leases

Demand Drivers: Medical real estate – which includes medical office buildings (MOBs), outpatient clinics, hospitals, and specialized facilities – is underpinned by the fundamental need for healthcare. As populations age and medical technology advances, healthcare services demand is only increasing. For example, U.S. healthcare expenditures are projected to reach $7.7 trillion by 2032 (a 73% increase from 2022). An aging demographic (the Baby Boomers in the U.S., and similar aging trends in Europe and Japan) means higher utilization of clinics, doctor’s offices, diagnostic centers, and senior care facilities. By 2040, about one in five Americans will be over 65, and they typically require more frequent medical visits. Additionally, healthcare delivery is shifting: there’s a broad trend of moving services out of acute-care hospitals and into outpatient facilities and neighborhood medical offices for convenience and cost efficiency. This “retailization” of healthcare – think urgent care centers, dialysis clinics, ambulatory surgery centers, etc. – means demand for well-located medical real estate in communities (often closer to where people live) is rising. Even in emerging markets in Asia, healthcare infrastructure is expanding to serve growing middle-class populations, though the ownership models can vary. Overall, healthcare is a necessity-driven sector, less subject to economic volatility: people need doctor visits and treatments in good times or bad, giving medical properties a level of occupancy stability that general offices or hotels may not have.

Supply Constraints: Medical facilities often require specialized buildings and regulatory approvals, which limits how quickly new supply can come online. A medical office building might need specific structural design (higher floor loads, special ventilation), proximity to a hospital or population center, and adherence to health regulations. Hospitals and large health systems sometimes develop their own real estate, but private investors play a big role in owning and leasing medical office space. Construction of new facilities has been steady but modest – for instance, in the U.S., even with robust development in recent years, the overall medical office vacancy fell from 2010 to 2023 by about 4 percentage points and is forecast to drop below 9.5% nationwide. This indicates that demand has kept pace or exceeded supply growth. There are also barriers to entry in many markets: it’s not easy to repurpose a regular office into a medical use due to build-out costs and zoning. Many prime healthcare properties are on hospital campuses or in medical clusters that are essentially built-out. Even off-campus, the best sites (near affluent or dense communities) get taken up, and then competition for remaining spots can be fierce. Another factor is that healthcare providers prefer stable locations to maintain patient loyalty and operational consistency, so they often sign very long leases, reducing churn in existing buildings. This creates a dynamic where existing medical properties become very valuable – investors covet them for the secure income, and tenants (healthcare providers) often renew leases rather than move. In Europe, some countries have a large portion of healthcare owned by the public sector, but private investment is growing in areas like private clinics, care homes, and life sciences labs.

Investment Thesis: Medical real estate is attractive for its high occupancy, long lease terms, and creditworthy tenants. Leases to healthcare providers (group practices, clinics, or hospital systems) commonly run 10 to 20 years with extension options, often on a triple-net basis (tenant responsible for expenses). This means an investor in a medical office building can enjoy steady rental income with built-in rent escalations, and the tenants (being essential service providers) are less likely to default or vacate. Even during economic downturns, medical tenants usually remain in place since healthcare demand persists. The cash flow durability of medical facilities has been proven over time – over the last decade, total returns from medical property portfolios have outperformed broader property indices, supported by those structural health demand trends. Moreover, healthcare real estate investment trusts (REITs) and funds have increasingly specialized in this segment. In 2023, healthcare and senior housing REITs were noted as one of the fastest-growing components in European real estate indexes, with a dedicated index delivering a 63.9% total return over 10 years (outperforming the broader market). Investors see an opportunity for above-average risk-adjusted returns here: cap rates on medical facilities can be higher than those on, say, prime multifamily, yet the risk profile is mitigated by stable occupancy and lease length.

Case Study – Market Momentum: Recent data and deals illustrate the strength of medical real estate. According to CBRE, the vacancy rate for U.S. medical office buildings hit a low in 2024 and asking rents have continued to rise, even with new construction in the pipeline. By mid-2024, investment activity in the sector picked up considerably – it was the first time since 2022 that annual transaction volume was growing and cap rates (yields) started to compress, indicating higher investor demand and confidence. One notable transaction was a joint venture of Remedy Medical Properties and Kayne Anderson acquiring a 37-property healthcare portfolio (from Broadstone) in 2023, exemplifying how large capital is aggregating medical assets. Kayne Anderson, in fact, has been one of the biggest players in U.S. medical office investments: since 2013, the firm has acquired over 32 million square feet of medical office space across 785 properties in 43 states. Such scale shows that specialized investors believe in the long-term value of these assets. Another angle is hospital systems doing sale-leaseback deals – selling their real estate to investors but remaining as long-term tenants – which frees up capital for the hospitals and provides buyers with a built-in tenant. Globally, we see similar trends: for instance, in India and China, private equity and sovereign funds are starting to invest in hospital and clinic platforms to tap into the healthcare growth, although those markets are still developing.

In sum, medical facilities as an investment offer a defensive play with steady income. The leases are often “bond-like” in their reliability (some running 15-20+ years), but unlike bonds, these properties also have upside from rent increases and property value appreciation. With healthcare being a universal necessity and many countries facing aging populations, the real estate that supports this sector has a strong underpinning. Investors seeking long-duration assets with inflation-hedging characteristics often find medical real estate fits the bill, and it serves as a diversification away from more cyclical property types.

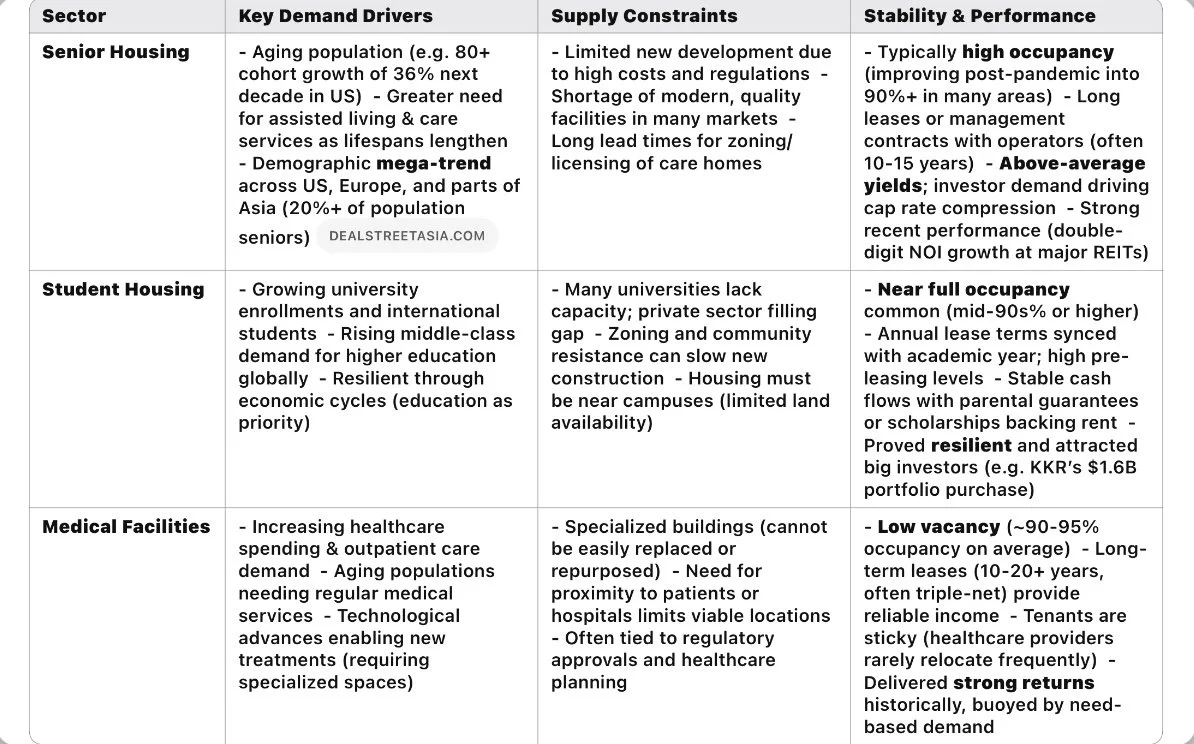

Comparison of Key Characteristics

To summarize the unique attributes of these three alternative real estate sectors, the table below highlights their demand drivers, supply dynamics, and typical investment features:

As the table shows, each sector draws its strength from broad, long-lasting trends (whether demographic or social) that translate into dependable real estate usage. At the same time, each faces natural limits on new supply, which helps existing assets maintain high occupancy and pricing power. These characteristics differentiate alternative sectors from more traditional real estate and contribute to their appeal for investors seeking stable and growing returns.

Conclusion: Long-Duration Opportunities for Above-Average Returns

Alternative real estate sectors like senior housing, student housing, and medical facilities are increasingly in the spotlight for good reason. They offer long-duration investment opportunities – assets that can generate income over decades, underpinned by demographic inevitabilities such as aging populations and expanding educational needs. Importantly, these sectors exhibit inherent supply constraints that create a landlord’s market: it is difficult to simply add a new hospital, senior community, or dorm in many locations, so well-positioned existing properties enjoy consistent demand.

For investors, these asset classes can provide diversification away from traditional office, retail, or residential holdings, and they often come with defensive qualities. For instance, alternative real estate assets have shown an ability to maintain or even grow earnings during periods of high inflation or slower economic growth, making them valuable in a balanced portfolio. They also align with socially significant needs – from caring for the elderly to housing the next generation of students to delivering healthcare – which can have the side benefit of impact or ESG considerations alongside financial returns.

Regionally, opportunities span the globe: North America leads in institutional investment and REIT presence in these sectors, Europe is catching up as aging and student mobility trends intensify (with high occupancy in key markets), and Asia – while culturally and structurally different in some cases – presents a vast emerging demand (e.g. rapidly aging societies in East Asia and a huge youth population in South Asia). Investors in the U.S. and Europe have already begun packaging these properties into REITs and funds, improving liquidity and access for individuals. In Asia, new partnerships and ventures are laying the groundwork for similar growth.

In summary, medical facilities, senior housing, and student housing each offer a compelling investment thesis: they are built on long-term demand that is unlikely to wane, face constrained supply, and can deliver stable income with potential for above-average returns as the rest of the market recognizes their value. As with any investment, due diligence is key – understanding local market dynamics, the quality of operators or tenants, and the regulatory environment. But the overall outlook for these alternative real estate sectors is optimistic. With macroeconomic conditions in 2025 cautiously improving (easing inflation and interest rate outlook) and capital markets increasingly open to non-traditional assets, savvy investors are positioning themselves to capitalize on these trends. By investing in these underappreciated sectors, one is effectively investing in the future needs of our society – a strategy that not only seeks profit but also supports critical services and housing for communities, achieving a win-win for portfolios and the public alike.

Sources:

• Ansarada Blog – Alternative real estate assets offer growth potential in 2025

• Ansarada Blog – Global student accommodation market size and growth

• JLL – 2025 Seniors Housing & Care Investor Survey and Trends

• Seniors Housing Business – InterFace Panel Insights (Hayden Spiess, Apr 2025)

• Multi-Housing News – What’s Next for Student Housing in 2025?

• ICEF Monitor – Global student housing demand vs. supply (Feb 2025)

• EPRA – Senior housing and healthcare real estate in Europe (2023)

• Clarion Partners – Positive Prognosis for Healthcare Property Sector (Oct 2024)

• CBRE – 2025 U.S. Healthcare Real Estate Outlook

• DealStreetAsia – Warburg Pincus ventures into South Korea’s senior housing (Mar 2025)

• Multi-Housing News – Harrison Street sells senior living portfolio

• Kayne Anderson – Medical Office Investments Overview

Report Generated by The ALFA Group